The Economic Carpet Doesn’t Match the Drapes

“The numbers don’t lie,” they say. This might be one of the biggest lies ever told. Numbers are often controlled by humans and because humans lie, the numbers can also lie. In this article, we’ll take a dive into the contradicting information delivered by mainstream media. Afterwards, hopefully we can do our own evaluation on how the US economy is performing.

The stock market is roaring to new heights, but ever increasing P/E ratios suggest they’re extremely overbought. Meaning, the price of stocks are rising much faster than the earnings, which result in increasingly higher Price to Earnings ratios. Some would argue that the higher ratios are due to expectations of future growth. In order words, we’re speculating. As Gordon Gekko so accurately stated in the movie Wall Street, “Speculation is the mother of all bubbles.”

An important truth to understand is that the stock market doesn’t represent the economy. The stock market is heavily influenced by many factors, true value being one of the least factors. I won’t go into details here; however, I will say that it is highly manipulated. I know the term “manipulated” is considered taboo on WallStreet, but when you consider allowable market transactions such as short squeezes, stock shorting and various other SEC approved shenanigans, it’s difficult to come to any other conclusion.

Big money can move the stock market up, down or sideways at will and make money in all scenarios. To understand this, you’d have to understand options trading, which is somewhat of a casino. We’ll dive more into this in a later article, but for now, the takeaway is to understand that the economy and stock market are not binary.

Next we’ll look at the job market. Thousands are losing their jobs on the daily, yet jobs reports and unemployment reports show strength. Microsoft, currently trading at all time highs, announced that they will do additional layoffs on top of the 10,000 employees they’ve already cut as of January 2024. In addition to the thousands of workers Amazon cut from their workforce in 2023, they plan to cut 27,000 more. Google also plans to cut 12,000 jobs this year. Macy’s will cut 2,000 jobs and close 5 stores. The list goes on and on of companies shuttering or laying off workers. These are just the companies we hear about. Mainstreet is also cutting jobs. If we think for one moment that they’re doing this because they’re expecting a “soft landing,” or because the US economy is in good shape, we’re being deceived.

Historically, there has never been a time where the Fed pumped excessive liquidity into the economy and took it out without wreaking havoc on the economy. The Fed knows a liquidity crisis is coming, that’s why Jerome Powell announced in December that they intend to cut rates in 2024. The Fed wouldn’t project rate cuts if they didn’t perceive a problem ahead. You can’t cut jobs by the thousands on a consistent basis and not have it affect GDP (Growth Domestic Product). Historically, on disinflation, for every one percent decrease in inflation, there’s a correlated 3% increase in unemployment. This factor has been fairly consistent throughout history, with the exception of 2022-2023. Must be some sort of magic or someone is cooking the books.

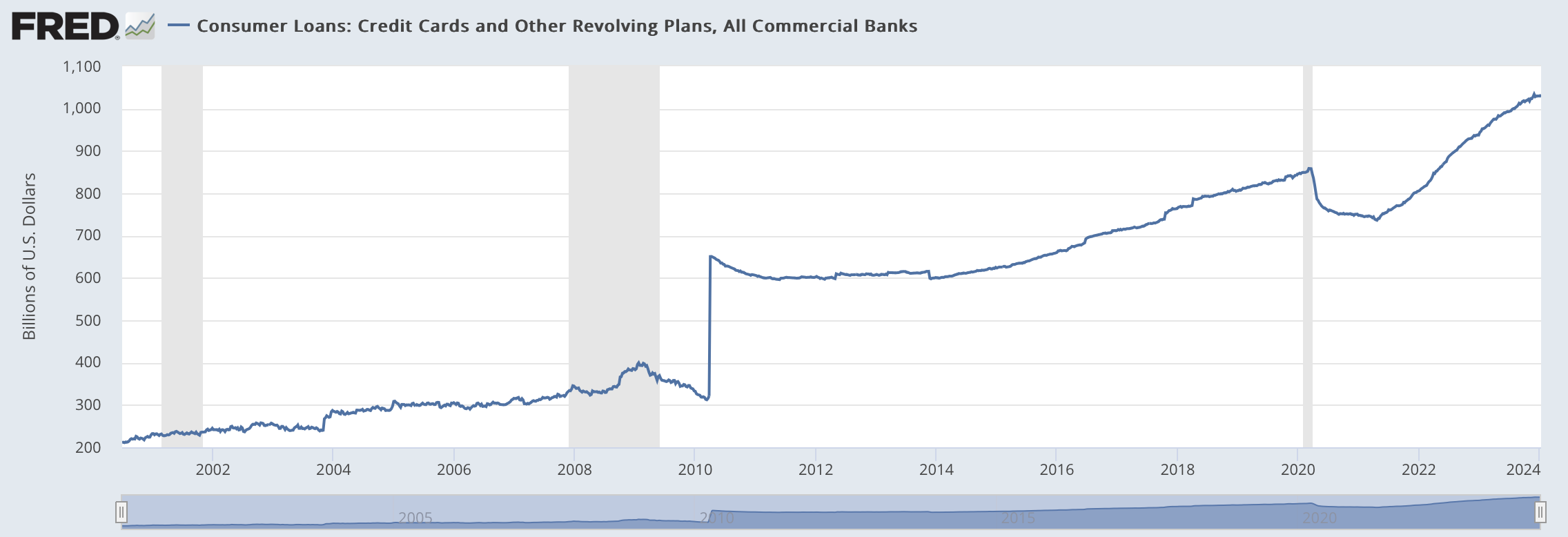

To add fuel to the fire, US consumer debt is the highest it’s ever been in history and growing month over month. With few exceptions, increasing credit card debt usually means, “I can’t afford my lifestyle.” As of December 2023, US consumer debt rose to $1.08 trillion. In 2019, that number was $927 billion. Had it not been for the stimulus money given out in 2020 through 2021, we would likely have witnessed US debt cycle down as defaults and bankruptcies ensued. However, the stimulus money kicked the can down the road. Now the correction will likely be even harder, because the debt is larger. If you’d like to learn more about debt cycles, Ray Dalio has an excellent video on YouTube called, “How the Economic Machine Works.” I highly recommend watching it.

According to FRED (Federal Reserve Economic Data), bankruptcies and credit delinquencies are rapidly rising, yet Jamie Dimon, CEO of Chase Bank, and other pundits say, “the US consumer is strong!” How can consumers be strong with rapidly increasing credit card debt? To add to that, many consumers are now turning to “buy now pay later” options, because their credit cards are maxed out, which is further increasing debt. I’d ask why the banks are still loosely providing credit under these circumstances, but that would require its own article.

I’d be remiss, if I didn’t state that the US is a debt based economy. Meaning, the majority of the money in circulation is credit rather than cash based. This allows you and I to spend more, which allows companies to make more and pay more. However, when access to credit dwindles, it has the opposite effect. At some point the banks will start to see rising defaults and bankruptcies as a threat to their own solvency. At which point, access will become more scarce resulting in less liquidity in the economy for all.

Not to travel back to the painful recession of 2009, but I vividly remember how the house of cards began to tumble in October 2008. In truth, it started tumbling the year prior. It just took a while to manifest itself in the stock market. My wife and I owned a fashion boutique at the time. Overnight, our customers disappeared. Credit card limits were reduced. A $10,000.00 limit became a $5,000.00 limit. If you owed $2,500.00 on said credit card, safely under the 33% where your credit takes a real hit, your credit took a huge hit. The reason is because you were now at 50% of your credit limit, rendering you as a higher credit risk, according to the credit bureaus. Higher credit card balances are a factor that would make it more difficult to get additional credit. Because credit is the name of the US economic game, everyone takes a hit when access goes away.

I don’t have a crystal ball and I certainly can’t tell you if or when the economy will crash. The powers that be can continue to play kick the can. The best I can do is look for similar circumstances over the course of history and how they played out. From there, I look at probabilities. Currently, the probabilities of a recession look to be inevitable. This article isn’t intended to scare you, but rather as a caution to prepare you. We can choose to bury our heads in the sand and continue with the illusion of bliss or get our houses ready for stormy weather. A perfect economic storm is brewing. Don’t get blindsided!

Written by:

Eric L. Lipsey | Founder | Owner

VENTRE Capital, Inc.

www.VentreCapital.com